Notification No.: 23/2025

Document Date: March 28, 2025

Applicable Act/Rule: Income-tax Act, 1961 & Income-tax Rules, 1962

Applicable Section/Rule: Form No. 3CD (Tax Audit Report)

Effective Date: April 1, 2025

The Central Board of Direct Taxes (CBDT) has issued the Income-tax (Eighth Amendment) Rules, 2025, bringing significant changes to Form No. 3CD, which is used for tax audit reporting under Section 44AB.

The key amendments include:

1. Clause 12 – The clause now includes 44BBC (Special provision for computing profits and gains of business of operation of cruise ships in case of non-residents), ensuring presumptive income reporting under this section.

2. Clause 19 – References to Sections 32AC, 32AD, 35AC, and 35CCB have been removed.

3. Clause 21(a) – A row read as “Expenditure incurred to settle proceedings initiated in relation to contravention under such law as notified by the Central Government in the Official Gazette in this behalf” shall be inserted after “Expenditure incurred to provide any benefit or perquisite”

4. Clause 22 – Substituted with:

(i) Interest inadmissible under Section 23 of the Micro, Small and Medium Enterprises Development Act, 2006 (MSMED Act); or

(ii) Total amount required to be paid to a micro or small enterprise, as referred to in section 15 of the MSMED Act, during the previous year;

(iii) Of amount referred to in (ii) above, amount –

(a) paid up to time given under section 15 of the MSMED Act;

(b) not paid up to time given under section 15 of the MSMED Act and inadmissible for the previous year.

5. Clause 26 (Section 43B Liabilities) – Clarifications in wording and scope of reporting for allowable deductions.

6. Clause 28 and 29 are omitted

7. Clause 31 – In Sub-Clauses (a) and (b) for item (ii) the following shall be substituted:

“(ii) Amount of each loan or deposit taken or accepted and code of the nature of such amount, as given in Note 1; [Dropdown to be provided]”;

8. Clause 31 – In Sub-Clause (c) for item (ii) the following shall be substituted:

“(iii) Amount of each repayment of loan or deposit or any specified advance and code of the nature of such amount, as given in Note 1; [Dropdown to be provided]”;

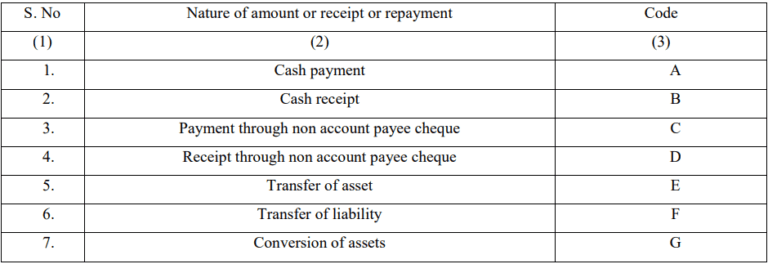

9. Note 1 – After Clause 31

“Note 1. – The code for the nature of amount/ receipt/ repayment is as below –

10. Clause 36B (New Insertion) – Share Buyback Reporting – Taxpayers must disclose details of share buyback transactions, including the amount received and cost of acquisition.

These amendments enhance tax transparency, particularly in areas like legal settlements, MSME payments, and financial transactions.

Disclaimer: The information contained in this Article is intended solely for personal non-commercial use of the user who accepts full responsibility of its use. The information in the article is general in nature and should not be considered to be legal, tax, accounting, consulting or any other professional advice. We make no representation or warranty of any kind, express or implied regarding the accuracy, adequacy, reliability or completeness of any information on our page/article.