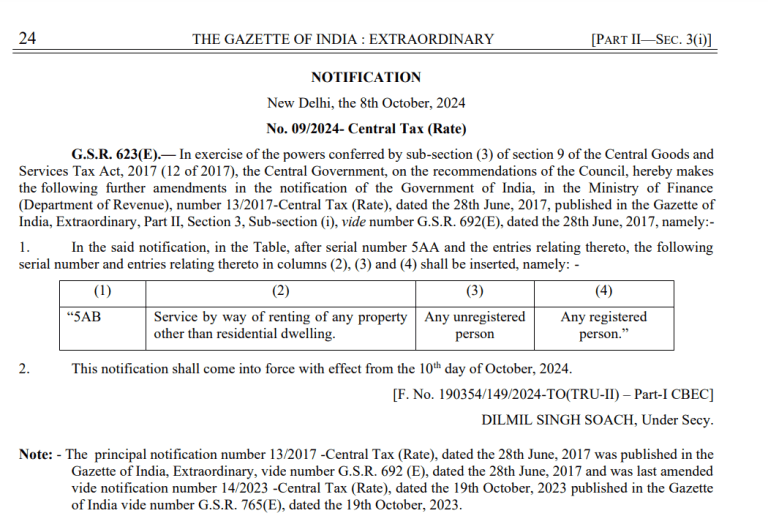

Notification No. No. 09/2024 –Central Tax (Rate)

Notification Date: 8th October 2024

Applicable Date: 10th October 2024

Relevant Act / Rule: Goods and Service Tax Act, 2017

Background: Certain services have been specified on which GST has to be paid under reverse charge mechanism. Earlier wide notification no. 13/2017 – Central Tax (Rate) dated 28th June 2017, Service by way of renting of residential dwelling to a registered person was covered under reverse charge.

Amendment: The Central Government on the recommendations of GST Council has made the amendment in notification number 13/2017 – Central Tax (Rate) dated 28th June 2017. Now the service by way of renting of any immovable property [* “any property” changed to “any immovable property” via Corrigendum published on 22 Oct 2024] other than residential dwelling by a un-registered person to a registered person, has also been covered under reverse charge mechanism.

Impact: Any transaction wherein an unregistered person is supplying service of renting of immovable property (other than residential dwelling) to a registered person, the said transaction shall be covered under reverse charge mechanism of GST and the recipient of such service (registered person under GST) shall be liable to deposit GST under revere charge.

The same can be understood by following example:

Nature of Service | GST Registration Status | GST under Reverse Charge | Person liable to deposit GST | |

Service Provider | Service Recipient | |||

Renting of Residential Dwelling | R | R | Yes | Service Recipient |

R | UR | No | Service Provider | |

UR | R | Yes | Service Recipient | |

UR | UR | NA | GST not leviable | |

Renting of Property other than Residential Dwelling | R | R | No | Service Provider |

R | UR | No | Service Provider | |

UR | R | Yes | Service Recipient | |

UR | UR | NA | GST not leviable | |

R: Registered

UT: Unregistered

The said notification will be effective from 10th October 2024.

Disclaimer: The information contained in this Article is intended solely for personal non-commercial use of the user who accepts full responsibility of its use. The information in the article is general in nature and should not be considered to be legal, tax, accounting, consulting or any other professional advice. We make no representation or warranty of any kind, express or implied regarding the accuracy, adequacy, reliability or completeness of any information on our page/article.