Background

The Maharashtra State Tax on Professions, Trades, Callings and Employments Act, 1975 was enacted to impose and collect a professional tax on individuals engaged in various professions, trades, and employments within the state. It was introduced as a revenue-generating measure permitted under Article 276 of the Constitution of India, allowing states to levy taxes on professions. The Act defines categories of taxpayers including salaried employees, self-employed professionals, and business owners, along with applicable rates and slabs. It also outlines registration, enrollment, deduction, remittance, and compliance procedures for employers and individuals. Overall, the Act serves as a fiscal tool for the state while standardizing the administration of professional tax across Maharashtra.

Applicability

This act shall be applicable to:

- Employer Liable to Register under Maharashtra Professional Tax

- Practising Professional Liable to Register under Maharashtra Professional Tax

- Company incorporated in Maharashtra

- Employer Liable to Register under Maharashtra Professional Tax

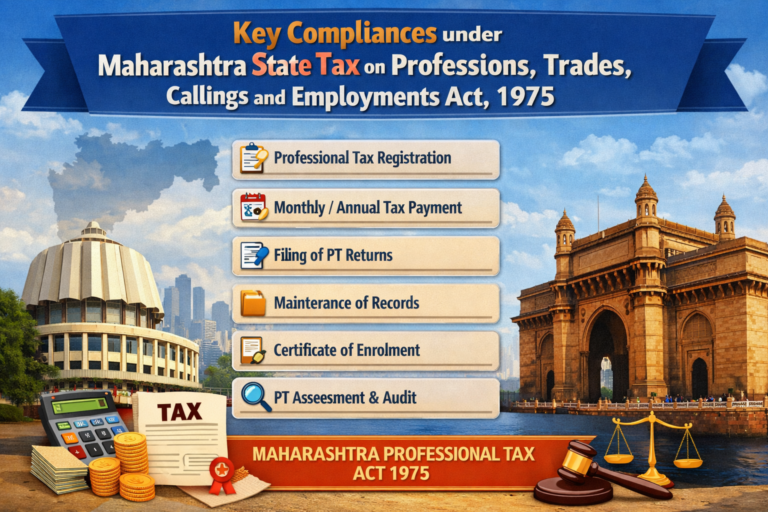

Compliance Requirements under the Act

- MTR-6 & Form III-B – PT Payment & Return by PTRC Holders (Maharashtra State Tax on Professions, Trades, Callings and Employments (Amendment) Act, 2020, Rule 11 of The Maharashtra State Tax On Professions, Trades, Callings and Employments Rules, 1975)

Tax is to be paid in Challan No MTR-6, and online return should be submitted in Form IIIB.

- Tax payment by PTEC Holders (Section 8 of Maharashtra State Tax on Professions, Trades, Callings and Employments (Amendment) Act, 2020)

Tax is to be paid in Challan no MTR-6

- Certificate of Registration (Section 5, Rule 3 of Maharashtra State Tax on Professions, Trades, Callings and Employments (Amendment) Act, 2020)

Every employer (not being an officer of Government liable to pay professional tax shall obtain a certificate of registration

- Certificate of Enrollment (Maharashtra State Tax on Professions, Trades, Callings and Employments (Amendment) Act, 2020, Section 5, Rule 4)

Every person who is engaged in any profession (business or service) excluding Partnership firm or HUF is required to get registered and to pay a profession tax

Certificate of Enrollment under Professional Tax as applicable on the Practising Professional in the State of Operations

- Company incorporated under Companies Act 2013 shall obtain both PTRC and PTEC (Section 5, Rule 4 of Maharashtra State Tax on Professions, Trades, Callings and Employments Act, 1975 )

All the companies incorporated under Companies Act 2013 shall after the date of commencement of Maharashtra State Tax on Professions, Trades, Callings and Employments (Amendment) Act, 2020, shall at the time of incorporation obtain PTRC and PTEC under the Act

- Exhibition of Certificate in Maharashtra (Rule 8 of Maharashtra State Tax on Professions, Trades, Callings and Employments Rules, 1975)

The holder of the certificate of registration or the certificate of enrolment, as the case may be, shall display conspicuously at his place of work the certificate of registration or the certificate of enrolment or a copy thereof.

- Preservation of Books of Accounts and Registers in Maharashtra (Rule 19A of Maharashtra State Tax on Professions, Trades, Callings and Employments Rules, 1975)

Every registered employer shall preserve all books of accounts, registers, including the register prescribed under rule 19 and other documents including vouchers and agreements relating to the activity of Professions, Trades, Callings or Employments for a period of not less than six years from the expiry of the year to which they relate

Penalty & Punishment

On contravention:

- Laible to pay S.I. besides Tax (Sec 9(2)

- Penalty for non-payment of tax @10% of the amount of tax due

Disclaimer: The information contained in this Article is intended solely for personal non-commercial use of the user who accepts full responsibility of its use. The information in the article is general in nature and should not be considered to be legal, tax, accounting, consulting or any other professional advice. We make no representation or warranty of any kind, express or implied regarding the accuracy, adequacy, reliability or completeness of any information on our page/article.